Why Republicans Lie About Health Care

The reality is they can’t create an alternative way to cover pre-existing conditions.

Gov. Scott Walker and State Sen. Leah Vukmir.

A lawsuit co-led by Wisconsin Attorney General Brad Schimel asks a federal court to declare unconstitutional the Affordable Care Act’s “guaranteed-issue and community-rating provisions.” The effect, if the judge agreed, would be to allow insurance companies to discriminate against people with preexisting medical conditions either by charging them more or by rejecting them outright.

Yet Gov. Scott Walker and US Senate candidate Leah Vukmir have reacted with indignation that their support for the lawsuit indicated less than fulsome sympathy with the plight of people with preexisting conditions trying to get health insurance.

The Journal Sentinel reported that Walker made a video in which he said:

My wife Tonette is a type 1 diabetic. My mother is a survivor of breast cancer. My brother has a heart condition. You see, covering preexisting conditions is personal to me. Plus it’s just the right thing to do. As long as I’m governor, I will always cover preexisting conditions.

Similarly, in a letter Vukmir defends her commitment to people with preexisting conditions.

Sadly, Senator Baldwin is lying to you and all Wisconsinites when she says I want to harm people with pre-existing conditions. As a nurse like you, I’ve made it my life’s work to help patients and save lives. I’m sure we can agree that nurses want to help their patients and ensure they have access to the best healthcare possible.

Are Walker’s and Vukmir’s protestations—and those of other Republican candidates who claim they will protect people with preexisting conditions—sincere? Or are they a cynical attempt to fend off criticism by referring to vague solutions? The answer may be irrelevant. Because there is no way they can fulfill their promise.

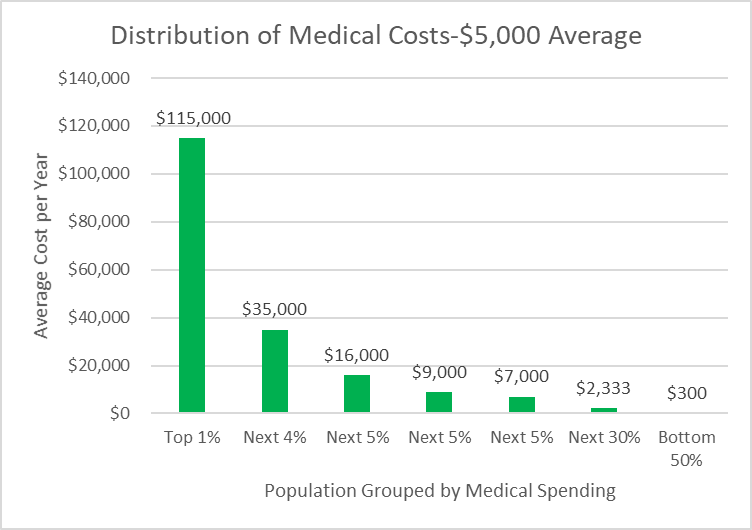

To understand why, it is useful to start with the basic challenge of the healthcare market: a small part of the population accounts for most of the cost. The next graph, based on estimates from the Kaiser Family Foundation, shows this starkly. The horizontal axis divides the population into seven groups, starting with the most expensive 1 percent on the left and ending with the least expensive 50 percent on the right.

The vertical axis, and the second number on top of each column, shows the health care cost per individual (adjusted to a market where the average cost is $5,000 per individual). As the graph shows, the average cost for those in the top 1 of costs is $115,000, dropping to $35,000 for the next 4 percent. Half the population, by contrast, manages to get through the year while spending almost nothing on healthcare—an average of $300.

Distribution of Medical Costs-$5,000 Average

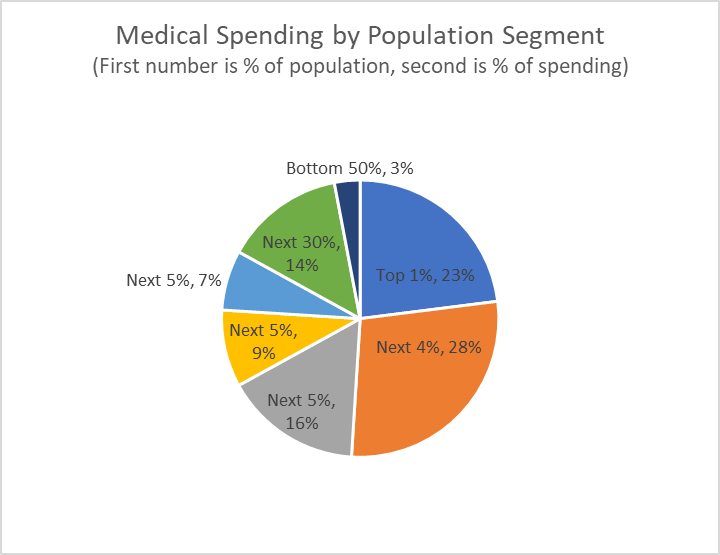

As the result of the skewed spending, the most expensive 1 percent of the population accounts for 23 percent of all money spent on health care, and the most expensive 5 percent of the population accounts for half of all medical spending. Then look at the next graph: the cheapest or bottom half of the nation’s population accounts for just 3 percent of all medical costs while the other half of Americans account for 97 percent of the medical costs.

Medical Spending by Population Segment

Let’s assume that no one in this market has health insurance. How would the market develop?

A potential insurer might calculate that medical costs average $5,000 and set a price—say $6,000—that covers its administrative costs and offers a nice profit. What could go wrong?

Even with no competitors for an insurance company, it may discover that its coverage is much more attractive to those on the expensive, left-hand side of the graph than those on the right. Thus, it may discover that its costs are much higher than it predicted.

Let’s assume, however, that this insurer manages to attract a mix of policy holders that looks like the population. This creates a very attractive opportunity for a competitor. If it can identify the 80 percent of the population that falls into the two lowest cost groups and offer a very attractive plan costing, say, $3,000 and still make money. The first insurer is then left struggling to pay for medical costs averaging $20,750 per person.Thus is born so-called “underwriting” in which insurers identify high-cost applicants and reject them, exclude their preexisting conditions from coverage, or charge them higher premiums. Success for the insurer has less to do with holding down costs than with identifying and avoiding the high cost policy holders.

Other insurers will take advantage of the situation by offering cheap junk insurance that excludes the most expensive medical conditions or quickly hits a spending cap. This largely describes the individual health insurance market prior to Obamacare.

Vukmir’s web site makes it clear that she is an advocate of allowing insurers to target particular segments of the population. Apparently, the alternative is Soviet-style central planning:

Leah supports replacing Obamacare with free-market solutions that will lower costs and premiums. For example, Leah would allow insurers to offer a wider variety of plans that fit the demands of patients and families, not government central planners. And she would support allowing individuals to buy insurance across state lines, increasing competition and choice.

To the extent that this paragraph encapsulates Vukmir’s health care policy, it is hard to envision a more hostile environment for making affordable, high-quality health insurance available to people with preexisting conditions. The more that insurance companies, including those in other states, can pick off low-cost members of the population, the harder it will be for people with pre-existing conditions. This conclusion is fundamental economics and neither Vukmir, Walker, nor their Koch-funded allies in Americans for Prosperity offer a solution.

The closest Vukmir comes to an alternative is to point to the former Wisconsin Health Insurance Risk-Sharing Plan. Unlike most state plans, Wisconsin’s managed to stay solvent. But its reach was limited. At its peak it enrolled about 24,000 people according to a Journal Sentinel article published when it was shut down. Its most popular plan had a $5,000 deductible. Both that and the premium made it unaffordable for most people. So scaling up this program to meet the need if Obamacare went away would require very substantial state subsidies.Rather than offering a realistic alternative to the ACA, Vukmir attacks Baldwin’s endorsement of a “Medicare-for-all” program. In a recent debate, she claimed it would “create chaos of epic proportions. … “I can’t believe Senator Baldwin wants to literally throw grandma off the cliff.” This is simple nonsense. Whether or not a single payer plan is best for the United States, there is no reason to expect it would lead to chaos. Plenty of other countries have successfully adopted single-payer plans.

In a debate with Tony Evers, Walker took a tack similar to Vukmir’s, claiming the state “can protect people with pre-existing conditions without protecting the failure that is Obamacare.” Again, he did not spell out how this might be done. Nor, for that matter, did he specify how Obamacare has failed.

When candidates insist they have a plan to solve a problem, but refuse to spell out how it would work, the safest conclusion is that magical thinking is at work. Never was this more clear than in the case of health care.

Data Wonk

-

Who Do You Trust to Conduct Elections Fairly?

Apr 6th, 2026 by Bruce Thompson

Apr 6th, 2026 by Bruce Thompson

-

Is Non-Citizen Voting a Real Threat to Elections in Wisconsin?

Mar 18th, 2026 by Bruce Thompson

-

How Global Climate Change Affects Milwaukee

Mar 11th, 2026 by Bruce Thompson

Mar 11th, 2026 by Bruce Thompson

What Bruce calls “magical thinking”, I call “good old-fashioned corruption and not caring about people.” Walker and Vukmir have no clue about how to get people health care/insurance without then going broke if things go bad, and they don’t care about that as long as insurance companies and the Koch/ALEC crew give them donations.

They both gotta go in 12 days.

I for about 6 months, I had my health insurance through the touted Wisconsin high risk plan (HIRSP). It covered by prescriptions for both my pre-existing conditions, which was good. However, I had between 6-18 month waiting period before the plan covered higher cost treatments. I had no other option, so I paid the premiums, which were substantial and prayed that either condition flared up.

Vukmir’s and Walker’s position of health care fails to acknowledge that the older we get, the more likely we are to develop health conditions. In other developed nations (like most of Europe and Canada), they recognize this fact and have shifted the focus of their health care systems to a more proactive approach — preventive care. The result is their populations are healthier even when diagnosed with such things as cancer and heart disease (they also have lower rates of such preventable conditions as type 2 diabetes). The kicker is that they healthcare systems cost less than here in the United States. Better results at a lower cost is the definition of efficiency.

Amen to the first 2 posts on this issue Neither Walker nor Vukmir have any credibility when they solemnly pledge to protect people with pre-existing conditions. Both have sided with insurance company lobbyists who have been lobbying to dismantle the Affordable Care Act’s pre-existing condition coverage. Neither W nor V have provided any specifics re how they would cover this group.

I have friends in Canada who love their health care system; moreover, they are appalled at how we let special interests deprive us of the benefits they enjoy. .

Republicans opposed Medicare when it was proposed by Democrats in the 1960’s. They have been trying to dismantle it since it became law. If you derive benefits now from Medicare or if you suspect that you could benefit from it in the future, vote for Democrats this November.