Payday Stores Charge Average Interest of 574%!

State is a leader in payday stores per capita, creates vicious cycle for low income people.

Latoya S. sits at her desk looking through overdue bills. Since 1998, she’s taken out close to 20 short-term payday loans. Photo by Marlita A. Bevenue.

One day last May, Latoya S. was walking her 6-year-old pit bull, Gucci, when he began to snarl excitedly at a strange man standing on the front porch of her brick, two-bedroom ranch home. As Latoya approached her home, the man spoke. “You Latoya?” She nodded.

The man came closer as the dog’s bark grew louder. He handed Latoya an envelope and said, “You’ve been served!” Latoya took the envelope and watched the man dash to an old, beat-up Ford Taurus. She pitched the crisp, white envelope into the bushes next to her front door and went in the house. She knew she owed a few thousand dollars to the Cash Store payday lending business in Grafton, and now she was being sued.

Latoya, who asked that her last name not be used, turned to the payday lender when she needed cash to pay her bills. And judging by the number of such operations in Milwaukee, there are many more people who find themselves in the same situation.

There are more payday lenders in Milwaukee as there are McDonald’s restaurants: 30 payday loan agencies inside the city limits and 25 McDonald’s, according to the corporate website. Check Into Cash, USA Payday Loans andAdvance America are a few of the convenient cash businesses planted in predominantly African-American and Latino communities, where many consumers in a financial crunch turn when they need money.

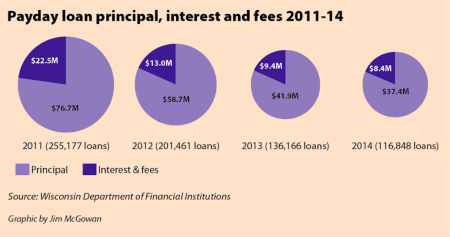

Payday loan principal, interest and fees 2011-14

The National Association of Consumer Advocates has deemed these businesses “predatory lenders.” Predatory lending is any lending practice that takes unfair advantage of a consumer by charging high interest rates and unreasonable fees and charges. Predatory lenders prey on minorities, the elderly, uneducated people and those who need quick cash for unexpected emergencies such as medical bills or car repairs.

Jamie Fulmer, senior vice president of public affairs for Advance America, takes issue with the term “predatory lenders,” blaming payday lending activist groups for misusing the label. “We offer consumers a product that is transparent and fully disclosed in the marketplace, and we do it in a simple, safe and reliable manner,” said Fulmer.

“If you peel back the onion and look at the actual facts associated with the products and services that Advance America offers, and you tie that together with the extremely high customer satisfaction and the low instances of complaints, I think it’s impossible to call us a predatory lender,” Fulmer added. Advance America runs 2,400 stores across the country.

No limit

Capitol Heights, Clarke Square, Sherman Park: payday loan agencies are scattered throughout communities occupied mainly by people of color. There are no licensed payday lenders in Whitefish Bay, Mequon, Brookfield, Wauwatosa, Shorewood, River Hills or Glendale.

“The only reason I believe some neighborhoods have these stores and some don’t is that the payday loan business owner wants to locate in poorer areas of the city,” said Patty Doherty, legislative aide to Ald. Bob Donovan. “People just are not very active and won’t bother to speak out against stores like this.”

According to Doherty, all payday loan stores in Milwaukee must get a variance, permission to deviate from zoning requirements, from the Board of Zoning Appeals. No areas in Milwaukee are zoned for payday loan businesses, so to open one the owner must convince the board that the business will not change the residential or commercial nature of the neighborhood.

Here’s how payday loans work: a customer who needs emergency cash takes out a short-term loan against his or her upcoming paycheck. In return, the person agrees to pay a high rate of interest on the loan. When the customer gets a paycheck, the agency automatically deducts the loan amount, plus a finance fee ranging from $15 to $30, directly from the customer’s checking account. The more money a customer borrows, the higher the finance charge.

Research conducted by The Pew Charitable Trusts in Washington, D.C., found that there are more payday loan stores per capita in Wisconsin than in most other states because its payday loan finance rates are so high, according to Nick Bourke, who directs Pew’s research on small-dollar loans.

“Wisconsin is one of seven states in the country that does not have a limit on payday loan rates. Right now, the typical payday loan in Wisconsin has an annual percentage rate (APR) of 574 percent, one of the highest rates in the United States — only Idaho and Texas have higher rates,” said Bourke.

“That rate is not just morally offensive, but it’s also far higher than necessary in order to make emergency credit available to people in need.”

‘Financial suicide’

Latoya, who grew up on the North Side of Milwaukee, came from a family where neither parents had a relationship with a bank. They both used local check-cashing stores to cash their bi-weekly paychecks. When a flier from Your Credit, a payday loan store on South 27th Street, came in the mail, Latoya decided to check it out. The flier promised quick cash, no credit check and lending options to build credit.

Latoya, then 19, was a freshman at UW-Milwaukee. She needed money for books and supplies, but didn’t want to ask her parents, who were already paying her tuition. Latoya went to the store and borrowed $75; two weeks later she paid back $150. Eighteen years later at age 37, she’s still paying off a payday lender after being sued for breaching the loan contract.

“Payday loan stores are parasites, period. In 2014, I took out a loan for $1,600, and ultimately had to pay back $5,000,” Latoya said. “They set up in the poorest neighborhoods in Milwaukee, preying on people who run into hard times. When your back is against the wall, trust me, you’ll do whatever it takes to keep your lights on, a roof over your head and food in your stomach.”

“Turning to a payday lender was financial suicide for me.”

It’s tempting to skip the small print on a lengthy payday loan contract, but for borrowers, those pages of legal disclosures are a must-read. The contracts reveal all the information that comes back to haunt borrowers later.

According to Amy Cantu, director of communications for the Community Financial Services Association of America, payday loan contracts guarantee that the lender is in compliance with the Truth in Lending Act (TILA), a federal law designed to protect consumers against unfair credit card and loan practices. TILA does not, however, place restrictions on how much a lender can charge in interest, late fees or other finance charges. The Community Financial Services Association of America represents payday lenders.

For nearly 20 years, Latoya continued to use payday lenders to help her out of ongoing financial difficulties. When she needed to replace the timing belt on her 1999 Chevy Malibu, she took out a $200 payday loan from Advance America, 8066 N. 76th St. When she got behind on her monthly car note and insurance payments, she borrowed $400 from ACE Cash Express, 1935 W. Silver Spring Drive.

“At one point, three cash stores were taking money from my checking account at the same time,” said Latoya. “That’s when I knew it was bad.”

Latoya didn’t limit her borrowing to in-store payday loan businesses; she also used online lenders. Online payday lenders offer the same services as in-store operations, providing an option for customers who prefer to submit a loan request through a website instead of in person.

“Once I discovered the online stores, I started using these exclusively,” she said “I knew online cash stores charged higher interest rates, but the process was quicker. I could fax or email my documents right from work and get the money the next day or in some cases, the same day.”

But according to a study by Pew Charitable Trusts, people who borrow money from online lenders are twice as likely to experience overdrafts on their bank accounts than those who borrow from a store. Plus, online-only lenders typically can avoid state regulations because the business operates entirely over the Internet.

According to Advance America’s Fulmer, “Much of the negative stigma associated with this industry stems from the online lenders that are not regulated at the state level. These businesses operate via the Internet, or some other offshore location, or in some cases they’re flat out scam artists,” said Fulmer. “There’s a difference between those of us who are regulated and audited by the state versus those lenders who aren’t.”

Payday loans are easier to secure than a traditional bank loan. According to PNC Bank’s website, to take out an unsecured loan, a customer would need proof of identification, bank account statements and recent pay stubs. A customer’s credit score can hinder the loan, and banks rarely make loan funds available the same day, or even within the same week.

“I applied for a loan from my bank and they denied me because of my debt-to-income ratio. The banker told me they prefer to loan larger amounts of money, repayable over time,” said Latoya, who has an active checking account with PNC Bank. “My bank couldn’t help me, so how else was I supposed to get groceries and pay my utilities?”

Article Continues - Pages: 1 2

Political Contributions Tracker

Displaying political contributions between people mentioned in this story. Learn more.

- June 13, 2019 - Patty Doherty received $700 from Bob Donovan

“People just are not very active and won’t bother to speak out against stores like this.” Really? You’re going to blame the residents AFTER some board has approved the store? People without the money in the first place? And then the city is going to let the corporation further feed upon them? Disgusting.

I find these companies to be slimy and morally wrong to take advantage of people… but I also hold the individuals responsible as well. Many of these people make extremely poor financial decisions. Latoya is an excellent example of that. No one making $57,000 a year should ever need to consider using one of these lenders.

Everyone falls on hard times, but that’s why you need to make good financial decisions and plan accordingly. Granted you can’t plan for everything, but most of the major things you can’t plan for wouldn’t be covered by these micro loans anyway.

One example of poor decision making is that even though I get paid more then her I would not blow $400 a month on a car payment. You can have a very reliable car for less than half of that even if you finance the whole thing.

What boggles my mind more… is that even after all these issues, she would still consider using them again! Unbelievable. You can’t legislate stupid.

I completely agree with you AG.

I’ve never used a Payday store, Check Into Cash, or any of these immediate cash stores – why – because I knew they were expensive. Not because I didn’t need the money. I’ve had many situations and many times where I needed some help.

———————————————–

“There are no licensed payday lenders in Whitefish Bay, Mequon, Brookfield, Wauwatosa, Shorewood, River Hills or Glendale.”

“This time she drove to the Cash Store in Grafton.”

“payday loan agencies are scattered throughout communities occupied mainly by people of color. ”

2013 Demographics – Grafton 94% white

————————————————————

“I applied for a loan from my bank and they denied me because of my debt-to-income ratio. The banker told me they prefer to loan larger amounts of money, repayable over time,” said Latoya, who has an active checking account with PNC Bank. “My bank couldn’t help me, so how else was I supposed to get groceries and pay my utilities?”

“Under the new CFPB rules, payday lenders also would have to verify and evaluate a customer’s debt-to-income ratio, the same process traditional banks use. They would be required to take into consideration a customer’s borrowing history when deciding whether the borrower is able to pay back the loan and still cover basic living expenses.”

“Asked whether she’d ever take out another payday loan again given her experience, she hesitated. “I hope to God that I don’t ever have to take out another loan. I’m going to try my best to avoid them, but if I do need the money I know it’s there.””

Uh-oh – If PNC Bank denied Latoya because of her debt-to-income ratio, and these cash stores are going to be required to do the same, and she gets denied there…..THEN WHAT????

————————————————————–

“……Latoya agreed to pay the amount over a six-month period, and walked out of the store with cash and peace of mind.”

“Latoya made nine payments on time to the Cash Store before falling behind. ”

And this is a reason that these loan stores ask for large interest rates. Because they don’t all get repaid in full, or on time.

“Latoya was sued by the Cash Store”

Does anyone have an attorney that works free?

——————————————————————–

“Every two weeks, Latoya would bring home a $1,700 paycheck after taxes. “My rent is $1,000, student loans are $594, my car note is $400 – that’s over $2,000 right there,” she said. “I still haven’t factored in utilities, car insurance, groceries or gas. I have no other option. I have no one to help me and they make it so easy to walk in the cash store, answer a few questions and walk out with cash money.””

Latoya brings home $1,700, after taxes, every 2 weeks = $3,400 a month – $2,000 between rent, student loans, car note,

That still leaves $1,400 a month for additional expenses.

—————————–

AG: “What boggles my mind more… is that even after all these issues, she would still consider using them again! Unbelievable. You can’t legislate stupid.”

Couldn’t agree more.