State Tax Burden Up, But Overall Burden Still Falling

Driven by rising income tax collections, Wisconsin’s state tax burden climbed in 2021 for the first time in a decade. Yet local and federal taxes as a share of income hit all-time lows during the pandemic and the total tax burden for state families and businesses is at its lowest level in at least a half century. Some taxes paid by middle-class families here remain relatively high, however, particularly the property taxes on a typical home.

For the first time in a decade, the state taxes paid by Wisconsin residents and businesses in 2021 grew as a share of income in the state. Yet the historically low levels of federal and local taxes in recent years have meant that the overall tax burden – and related spending on public services – have kept dropping for Wisconsinites.

The increased state tax burden did not result from higher tax rates, but instead reflected factors such as a surge in economic activity as the state emerged from the worst of the pandemic. In fiscal year 2021 (the 12 months ended on June 30), state sales tax revenues rose by more than 9% – the most in 37 years. Corporate income and franchise tax collections rose by 59.2% – the most in our records going back to 1960. Individual income tax revenues for the state rose by 6.2% – the most since 2013. In fact, total state tax collections from all sources grew 9.2% in 2021, the largest annual increase since 1984.

For decades, the Wisconsin Policy Forum and its predecessor, the Wisconsin Taxpayers Alliance, have been tracking every local, state, and federal tax paid within the state – from those on vaping products to motor fuel. By comparing tax collections to the collective incomes of state residents, we can gauge the impact of these taxes on the families and businesses who are responsible for them.Not surprisingly, the growth in state tax collections outpaced the 5.2% increase in personal income in Wisconsin in calendar year 2020 (the most recent year available). The figures on personal income include wages and salaries, interest and dividend income, and transfer receipts to individuals from the government – a major factor during the pandemic. As a result, state taxes grew to 7% of personal income in 2021, up from 6.7% the previous year.

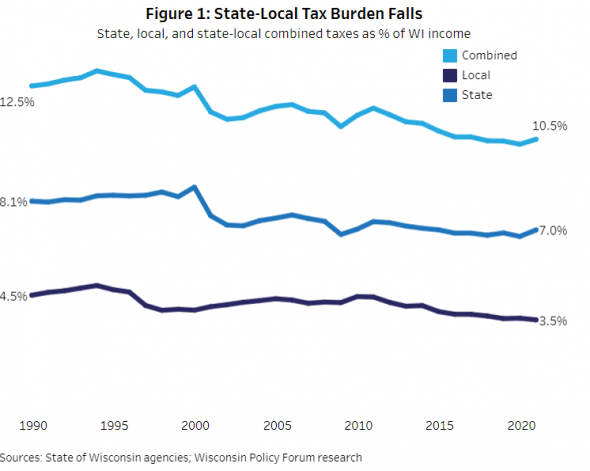

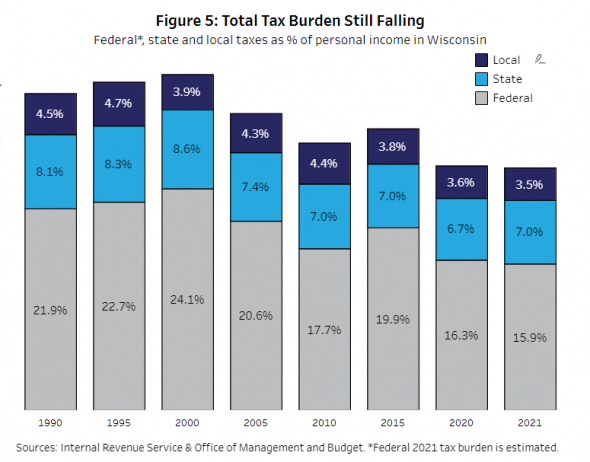

As a share of income, property and other local taxes fell in 2021 to 3.5%, down from 3.6% the previous year to the lowest level since at least 1970. Overall, combined state and local taxes rose to 10.5% of income in Wisconsin in 2021, up from 10.3% in 2020 but still the fourth-lowest year in our records (see Figure 1).

The tax burden was even lower if federal taxes are considered. Federal tax collections from Wisconsin have fallen since 2017 due both to the passage of the Tax Cuts and Jobs Act in December of that year and the impact of the pandemic on the economy. At the same time, the incomes of state residents were propped up by multiple rounds of federal aid – with some unemployment insurance payments excluded from federal income taxes. The result, as we will discuss, has been a falling federal tax burden and the lowest level of overall taxation as a percentage of income for Wisconsin residents since at least 1970.

This drop in the total burden does not mean, however, that tax liabilities have dropped for all Wisconsin residents equally or that certain taxes do not remain relatively high for lower and middle-class families. To help explore those nuances, this report will also look at effective property tax rates for the typical home in Wisconsin as well as income tax rates for filers at different income levels.

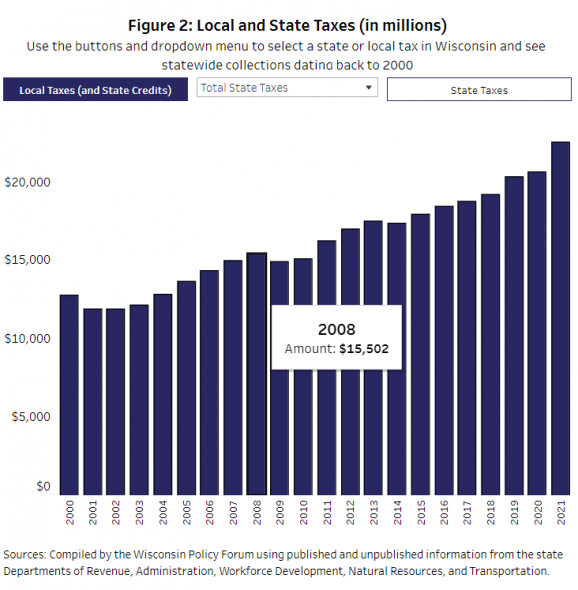

Total state and local taxes in Wisconsin rose to $33.96 billion in 2021, up 7.1% from $31.7 billion the previous year. Figure 2 allows readers to explore figures on individual taxes, which are also discussed below.

Since personal income rose more slowly than combined state and local tax revenues in Wisconsin, the overall tax burden rose. Yet the actual impact of state and local taxes as a share of income remains relatively modest compared to past years. As the Forum recently reported, 2019 U.S. Census Bureau figures show Wisconsin’s state and local tax burden is also below the national average and its ranking at 23rd highest among the 50 states has never been lower in data going back to 1994.

STATE TAXES

State tax collections grew at their fastest rate in more than a generation to $22.61 billion in 2021, up from $20.71 billion the previous year. The increase reflects a combination of factors, including recovery from the COVID-19 pandemic, the effect of federal stimulus, and other federal and state actions, court decisions, and policies. Those include ensuring that certain online and out-of-state retailers would collect state and local taxes on those rapidly growing sales and stepping up efforts to audit out-of-state companies.

In terms of general fund revenues such as income taxes (individual and corporate), sales taxes, and excise taxes, Wisconsin saw an 11.6% rise in fiscal 2021. That increase was still somewhat below the estimated average for all states of 12.8%, according to a recent report by the National Association of State Budget Officers (NASBO). As we will discuss, major tax cuts also will be taking effect next year in Wisconsin that should limit state collections and potentially lower the state tax burden moving forward.

Individual Income Tax

After falling in 2020 for the first time in six years as a result of the pandemic, revenue from the individual income tax – the largest state tax – rebounded sharply as part of the overall economic rebound from COVID-19. Revenues from the individual income tax rose 6.2% to $9.28 billion in 2021. That was considerably less, however, than the estimated 14.7% increase nationally reported by NASBO.

Despite the overall increase, collections for the 2020 tax year were lowered by $256.4 million because of a provision in state law that requires additional sales tax revenues from the customers of certain online and out-of-state businesses to be used to cut income tax rates. These lower rates in the first and second brackets have been extended into 2021 and future years.

In the 2021-23 budget, Gov. Tony Evers and lawmakers approved massive cuts of more than $1 billion in state income taxes in fiscal year 2022 alone. In addition, Evers and legislators in February enacted a projected $563.1 million in tax cuts for recipients of Paycheck Protection Program loans and others plus $31.3 million in additional spending on tax credits. Together, these tax decreases are among the largest at the state level in recent memory and promise to significantly impact state tax collections in future years.

Sales Tax

The second largest source of state revenue is sales and use tax collections. In 2021, revenues from sales tax collections grew 9.2% to $6.37 billion. That was the largest year-over-year increase since 1983 – a year that immediately followed the Legislature’s increase of the sales tax rate from 4% to the current 5%. It also outpaced the estimated national average of 6.9% as reported by NASBO.

The increase resulted in part from the reopening of certain businesses that are key for the sales tax such as bars, restaurants, and hotels. It also likely reflected an ongoing shift in consumer spending during the pandemic toward goods (generally subject to the sales tax) and away from services (often exempt from sales taxes). Last, sales tax revenues have been boosted in recent years by a 2018 U.S. Supreme Court decision and a 2019 state law that helped ensure that growing online retailers remit sales taxes from their consumers. A rise in state auditing of certain businesses also may have contributed.

Corporate Income Tax

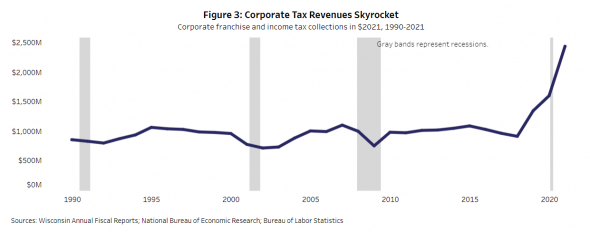

Corporate franchise and income tax revenues continue to grow at an astonishing rate – rising by a record 59.2% in 2021 to $2.56 billion (see Figure 3). That was the biggest increase in WPF’s data going back to 1961, exceeding the 2019 increase of 49.7% and the previous record of 51.8% in 1964.

The 2021 growth in Wisconsin easily surpassed the estimated national average of 34.1% in the NASBO data, though a number of other states did report greater estimated increases this year. State corporate tax collections here are now at their highest level on record even after adjusting for inflation. As we will discuss, however, the overall state and federal taxes paid by corporations are likely lower after factoring in changes at the federal level.

While it may have been expected that the economic disruptions from COVID-19 would have a strong impact on revenues, there are several factors that likely drove up corporate tax collections. As previously noted, one is the massive levels of federal pandemic aid to both corporations and individuals, which helped boost income for both. The pandemic also led to delayed tax filing and payment dates for corporations toward the end of fiscal 2020, which in turn pushed some payments into 2021. Other factors include an increase in state auditors and changes to the federal and state tax code that appear to have led more business entities to file and pay their taxes at the corporate level.

Excise Taxes

As noted in a recent Forum report, alcohol sales in Wisconsin shot up during the pandemic and tax collections rose by their largest percentage since 1972 – a year that included an increase in wine and liquor tax rates and a lowering of the drinking age. Liquor and wine tax revenue grew 17.9% to $64.6 million, while beer tax revenue increased 10.7% to $9.4 million.

Cigarette tax collections – an important source of revenue for Wisconsin compared to other states nationally – declined 2.6% to $509.8 million in 2021. Tax revenue for other tobacco products such as chewing tobacco and loose-leaf tobacco grew by 1.5% to $92.7 million.

In 2020, the state enacted a new tax on vaping products at a rate of five cents per milliliter of liquid or other substance. Although total vaping taxes increased 18.0% to $1.6 million in 2021, collections were still well below the $3.2 million forecasted at the time of enactment.

Gas and Transportation Taxes

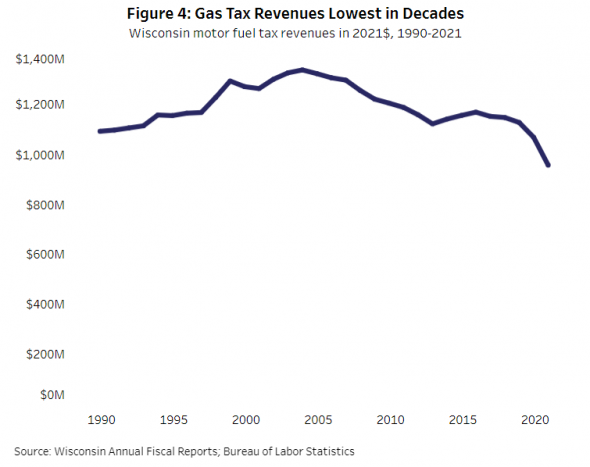

Gas tax collections continued their decline from 2020 into 2021 as a result of reduced driving from the pandemic. Total revenues from motor fuel taxes declined an additional 6.2% to $959.4 million – the lowest level in decades if adjusted for inflation (see Figure 4). Much of this may reflect a rise in the number of people working from home as well as continued constraints on business and vacation travel.

Other transportation revenues include driver’s license, vehicle registration, and limo and car rental fees. In contrast with other state taxes discussed previously that go into the state’s general fund, transportation revenues go into a segregated fund and are only used for transportation spending.

Revenue from these other transportation fund sources rose in 2021. Vehicle registration fee revenue increased by 8.5% to $910.2 million while driver’s license revenues also rebounded after falling in 2020 to $40.7 million in 2021, an increase of 4.3%.

Unemployment Tax

Unemployment tax revenue decreased 15.0% in 2021 to $456.9 million, the lowest level since 2002 even without adjusting for inflation. Collections have now fallen 61.5% from their 2012 peak of nearly $1.2 billion. State payroll tax rates for unemployment ratcheted down automatically in the years leading up to the pandemic, as the reserves in Wisconsin’s jobless fund grew to $2 billion by the end of 2019.

The Legislature and Evers stepped in to prevent that tax increase, however, by approving a $60 million transfer from the state’s general fund to the unemployment fund in both 2022 and 2023. That begins the process of replenishing the jobless fund and delays any tax increase for at least two more years. Future rate increases still might occur, however, if the fund’s reserves do not rebound adequately. That remains a real possibility (if not a likelihood) given the roughly $1 billion loss from the pandemic.

LOCAL TAXES

Total local tax collections rose 3.3% to $11.35 billion in 2021, up from $10.98 billion the previous year. While the increase was not insignificant, it was a slowdown from 2020. Because growth in personal incomes exceeded the growth in collections, it also produced yet another decrease in the local tax burden to 3.5% – the lowest level in our half century of records.

The lower tax burden largely reflects successful efforts by state officials over the past decade to hold down property taxes, the largest single tax in Wisconsin and one that accounts for nearly all local taxes. In recent years, local governments have seen some increases in collections from much smaller taxes such as vehicle registration fees and county sales taxes.

Property Tax Collections

Gross property tax collections on bills sent out in December 2020 and paid into 2021 grew 3.4% to $12.02 billion. The state lottery credit also fell so actual net taxes owed by property owners after subtracting state credits increased by 4.2% to $10.69 billion. The percentage growth in net property taxes was the highest since 2010. Property tax collections appear to have remained stable during the COVID-19 pandemic despite early fears that they could be affected by potential challenges from business failures and home foreclosures.

The three state property tax credits – the lottery, school levy, and first dollar credits – reduced local tax levies by a combined $1.32 billion in 2021, a 2.9% decrease from the previous year. This was due to a 12.6% decrease in the lottery credit to $236.1 million. The school levy and first dollar credit remained relatively stable at $940 million and $148.0 million respectively.

In the 2021-23 budget, Evers and lawmakers boosted state aid to schools without increasing limits on overall school revenues, which is curbing growth in property taxes levied by school districts. The governor and legislators are also working on lowering personal property taxes, which similarly would help to keep overall levies in check. Factors that could offset those moves, however, are continued pressure from school referenda and rising municipal and county debt payments.

Sales Taxes

In addition to the 5% state sales tax, counties can opt to impose an additional sales tax of 0.5%. Despite fears that the pandemic would depress county sales tax revenues, collections grew by a robust 5.9% in calendar 2020 to $479.9 million. (Our reports use calendar year data for the county sales tax.)

One reason for the growth in revenues was the implementation of a sales tax by both Outagamie and Menominee counties in the spring of 2020. To date, only four of Wisconsin’s 72 counties (Manitowoc, Racine, Waukesha, and Winnebago) have not adopted a sales tax. Without the addition of these two new counties, statewide revenues would have grown by 2.3%.

Going back to 1996, five counties (Milwaukee, Racine, Ozaukee, Washington, and Waukesha) had collected a 0.1% sales tax to pay for what was then known as the Miller Park baseball stadium. However, this tax officially ended in March of 2020, resulting in zero revenues being recorded for 2021.

Wheel Taxes

Municipalities and counties have the option to enact a local vehicle registration fee, also known as a “wheel tax,” that must be used for transportation-related spending. Fees adopted by local governments have ranged between $10 and $40 annually.

Total revenue from local wheel taxes rose 12.1% to $62.8 million in 2021 as collections continue their aggressive growth. For more on this trend, see this Forum brief from November.

Room, Premier Resort, and Local Expo Taxes

In general, municipalities have the ability to enact hotel room taxes of up to 8% as long as 70% of the revenue from these room taxes is used for promoting tourism in the municipality. In 2019 – the latest year with a final statewide amount available – total revenue from room taxes grew 4.1% to $121.5 million. This figure does not account for the severe impact of COVID-19 on statewide collections.

In Milwaukee, state authorization to levy a room tax is granted to the exposition district supporting the Wisconsin Center. Collections for the district took a massive hit due to COVID-19. Revenues from its taxes on hotel rooms, food and beverage sales, and car rentals declined 50.1% to $17.8 million.

Additionally, seven Wisconsin municipalities that are tourist destinations can impose what are known as premier resort area sales taxes on certain sales by certain businesses. The impact of COVID-19 was evident in these tourist areas as revenue from this tax dropped 22.2% to $8.1 million in calendar year 2020.

Federal Taxes

The federal tax burden for Wisconsin taxpayers is also at its lowest level in a half century. Though federal taxes are not the main focus of this report, they comprise the majority of taxes paid by Wisconsinites ($51.6 billion estimated in federal fiscal year 2021 compared to $33.96 billion in state and local taxes).

We estimate that growth in federal tax collections in Wisconsin was outpaced by personal income over the most recent year, leading the federal tax burden to fall to an estimated 15.9% of income. In 2020 – the most recent year for which we have actual tax figures for Wisconsin – the federal tax burden was 16.3% of income. Those figures are the lowest in our records going back to 1970. However, with that lower tax burden and additional federal pandemic spending came unprecedented federal budget deficits over the past two years.

As a result, the combined 2020 tax burden for federal, state, and local taxes was the lowest in our records and the projection for 2021 – which is still subject to revision – would be lower still if the estimate holds (see Figure 5).

The vast majority of federal tax collections in Wisconsin (92.3% in 2020) consist of individual income and payroll taxes. The next largest portion is corporate income taxes at 5.8% or $2.94 billion in 2020. That share was as high as 12.1% in 2014 ($6.02 billion) and has fallen since the December 2017 passage of the corporate tax decreases contained in the federal Tax Cuts and Jobs Act. Despite the increase in state corporate payments, this drop of more than $3 billion in federal taxes suggests that collectively, corporations with a Wisconsin nexus are likely paying less in combined state and federal corporate taxes in 2020 than they were paying prior to the TCJA.

Nuances behind the tax Burden

The decline in the overall tax burden in Wisconsin to below the national average has meant lower taxes for taxpayers collectively. Yet some individuals and businesses have benefited more than others. For example, decreases in the state’s personal property tax mainly benefit commercial properties and not homeowners, while decreases in income taxes due to a major tax credit for manufacturing and agriculture have been limited to business owners and shareholders in those industries.

In reviewing the state’s three largest taxes, the Forum has noted in the past that property and income taxes for middle- and upper-income families in Wisconsin generally tend to be relatively high compared to the rest of the country. Income taxes for low-income families tend to be lower and sales taxes in this state are relatively low for all taxpayers.

Property Tax

A study from the Lincoln Institute of Land Policy and the Minnesota Center for Fiscal Excellence helps compare the property taxes paid by homeowners across the country. The annual report looks at taxes at varying home values for both the largest municipality in each state and a representative small community – the cities of Milwaukee and Rice Lake in the case of Wisconsin.

In Milwaukee, 2020 property taxes on a $150,000 home were $3,646. That was nearly 83% higher than the national average for the same value home of $1,995, placing Milwaukee fourth highest among the 50 largest cities by state. The rank was the same for the taxes on a $300,000 home. Compared to other large cities, Milwaukee also ranked sixth highest nationally for its effective tax rate on a median-valued home.

A $150,000 home in Rice Lake had a tax bill of $3,091 in 2020. That was 58% higher than the national average of $1,960 and ninth-highest among the 50 representative smaller communities. The figures for a home valued at $300,000 were once again similar.

As the Forum has pointed out, Wisconsin’s residential property taxes are among the nation’s highest because of several policy decisions made by state officials over generations. The state relies heavily on property taxes to fund local government and less on sales and other taxes; many types of property such as manufacturing equipment and farm and forest land have had their taxes either eliminated or greatly reduced; and the “uniformity clause” in the state Constitution requires different classes of properties to be taxed in a uniform fashion. That means state and local officials in Wisconsin cannot give preferential tax treatment to homeowners to the same degree as some other states.

The study by the Lincoln Institute and Minnesota Center for Fiscal Excellence helps illustrate this final point by listing how much effective tax rates on commercial properties exceed those on residential properties for each state. For the largest cities in each state nationally, the effective tax rate on commercial properties was on average 76.6% greater than it was on residential properties. For Milwaukee, effective rates on commercial properties were only 6.9% higher than those on residential properties. That meant that among the largest cities in the country, Milwaukee homeowners had some of the smallest relative advantages and commercial owners had some of the smallest disadvantages.

Income and Sales Taxes

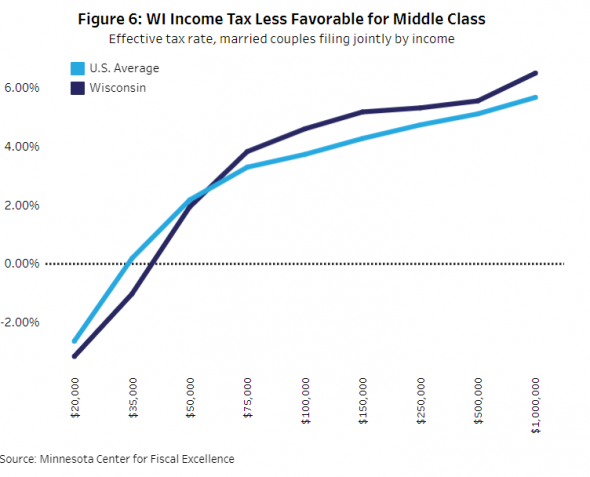

Among states with an income tax, Wisconsin has one of the more progressive systems, another study from the Minnesota Center for Fiscal Excellence has shown. A progressive tax system is one in which those with higher incomes pay a greater percentage of their income in taxes compared to those with low incomes.

In 2018, a Wisconsin married couple filing jointly with $20,000 in income paid no state income tax, and actually received a payment of $629 from the state due to the earned income tax credit. That ranked 31st highest among states in terms of the taxes owed (or payment received). Note that the definition of income used in the study includes some income that is not subject to taxes.

A similar couple earning $50,000 paid $975 in taxes – roughly 1.95% of income. That ranked 25th-highest nationally. The percentage of income paid as taxes continued to rise for similar couples earning more, with a couple making $100,000 paying 4.61% of their income in taxes, or $4,613. That was fifth highest nationally.

As Figure 6 shows, that means Wisconsin tax filers at the lowest incomes were paying less in taxes than similar couples nationally and receiving more in credits. On the other hand, those in Wisconsin with $75,000 or more in income were paying more in taxes. The same broad trend is true for single and head of household filers.

Last, Wisconsin relies less on sales taxes to fund state and local governments than most states. The state has relatively few local sales taxes and unlike some states also exempts food from the tax. That means sales taxes are a smaller burden for taxpayers of all income levels in Wisconsin. However, the lower sales taxes represent a somewhat greater benefit to those with the lowest incomes since their sales tax payments comprise a larger portion of their incomes than those of greater means.

Conclusion

After a decade in which legislators in the state Capitol have put considerable focus on lowering taxes and the 2017 adoption of a major tax overhaul at the federal level, the combined local, state, and federal tax burden has never been lower for Wisconsin residents in our records. Though state tax collections surged in 2021 with the gradual reopening of the economy, a fresh round of massive tax cuts at the state level also should help to hold down tax revenues in future years.

Yet, despite the clear downward trend in Wisconsin’s overall tax levels over the past generation and particularly the past decade, taxes remain a highly contentious topic among state and local policymakers and many citizens in Wisconsin. That may be because property and income taxes – the two largest and most salient taxes for ordinary individuals – remain relatively high for homeowners and middle- and upper-income families in Wisconsin. The state’s relatively low sales taxes may fail to register with many taxpayers since they are paid in small amounts over the course of the year rather than in one lump sum.

In terms of forecasting how the tax burden may evolve in the future, the current legislative session provides helpful clues. Faced with the welcome surprise of tax projections that were more than $4 billion above previous expectations, lawmakers last summer prioritized property and income tax cuts over public spending in areas such as K-12 and higher education and local services such as public safety, libraries, and parks. In particular, the Legislature has sought to limit both local property taxes as well as state aid payments to local governments.

For now, local governments are leaning on federal pandemic aid to help manage the constraints on both property taxes and state aid. An additional infusion of federal infrastructure funds may also provide further relief for tight budgets and the growing problem of rising backlogs in capital projects for some local governments such as those in Milwaukee.

In the long term, however, a continued focus on lowering Wisconsin’s tax burden may bring with it diminished public services, particularly at the local level. Already, for example, the state has seen its per pupil spending on K-12 education fall from the top 10 nationally to below average.

A decade ago, the state helped school districts and local governments manage tighter budgets by repealing most collective bargaining for most public employees. Today, if they wish to continue their tight controls on the revenues of local governments and school districts, state leaders may wish to consider new ways to help their local counterparts manage their challenging finances.

Those might include providing greater state assistance to local leaders who are seeking to gain new efficiencies through technology or enhanced service sharing or consolidation; or using the state’s improved financial condition as an opportunity to consider new or enhanced forms of state aid. The alternative in the long run may be lowered service levels at a time when the pandemic has created new challenges at all levels of government.

NOTE: This press release was submitted to Urban Milwaukee and was not written by an Urban Milwaukee writer. While it is believed to be reliable, Urban Milwaukee does not guarantee its accuracy or completeness.

Recent Press Releases by Wisconsin Policy Forum

Small Business Creation Rose Post-Pandemic; Expansion Remains Key Challenge

May 28th, 2026 by Wisconsin Policy ForumReport finds small business disparities rooted in business size, industry, and location

Proposed MPS Budget Resolves Fiscal Shortfall but Leaves Another Looming Gap

May 27th, 2026 by Wisconsin Policy ForumBudget is balanced for 2027, but large deficit forecast for future years

Value Judgment: A Look at Property Assessment in Milwaukee County

Apr 13th, 2026 by Wisconsin Policy ForumCurrent approach has cost upsides, but may affect assessment accuracy, uniformity