How Will Trumpcare Affect Wisconsin?

The bottom line: worse health and 1,000 additional deaths per year.

Donald Trump. Photo from whitehouse.gov.

After several months of secret meetings the U.S. Senate leadership released its version of the bill to replace Obamacare, called the Better Care Reconciliation Act of 2017. The Congressional Budget Office (CBO) projects that 22 million people now covered by Obamacare would lose their coverage. How would it affect Wisconsin?

The next graph shows the elements that go into CBO’s estimate that 22 million would lose coverage. Roughly seven million of this loss comes from changes in the “nongroup” market, those purchasing insurance on their own or through the Obamacare exchanges. Although these exchanges have received the most attention, about twice as many people—15 million—would lose coverage because of proposed changes to Medicaid, especially its conversion to block grants that would be capped at less than the medical inflation rate.

CBO Estimate of Uninsured Americans

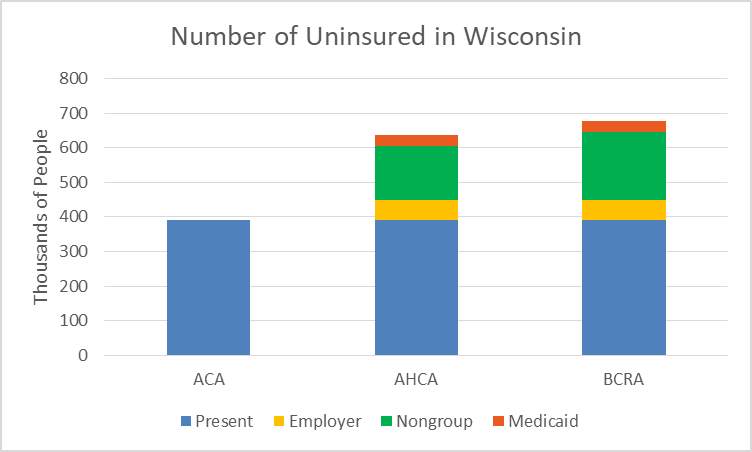

While the CBO has not broken down the projected coverage decrease for each state, the Urban Institute concludes that in Wisconsin, about 286,000 more people are expected to be uninsured under the Senate health-care bill than under Obamacare in 2022, as shown on the following chart. There are some differences between the estimates from the CBO and the Urban Institute; for example, the latter projects that 24 million people would be left without insurance under the Senate bill. Yet it also estimates that two thirds of this increase would come from people losing coverage from Medicaid. What explains the Wisconsin difference?

Number of Uninsured in Wisconsin

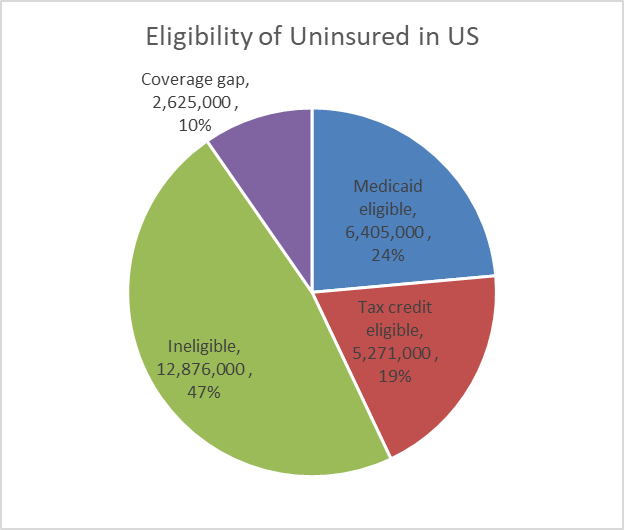

A place to start is with the coverage gap, people who made less than the Federal Poverty Line, but more than their state’s cap on family income eligible for Medicaid. According to the Kaiser Foundation, as shown in the graph below, nationally about 10 percent of the uninsured is due to the coverage gap. Every one of the states with a coverage gap turned down the Obamacare offer of additional funding to plug this gap.

Eligibility of Uninsured in US

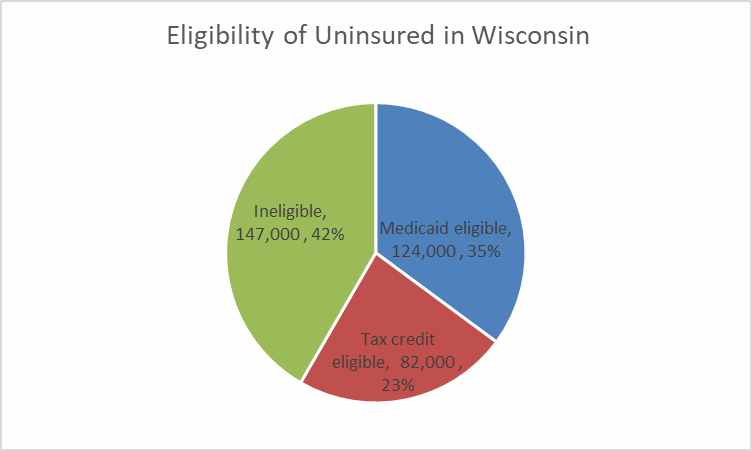

Wisconsin was the exception. It turned down the funding but closed the coverage gap. Instead it moved people whose income exceeded 100 percent of the Federal Poverty Level (FPL) out of Medicaid and encouraged them to buy private insurance on the Obamacare exchanges. Doing so made room for more people under the FPL to get on Medicaid (mostly adults without children).

Compared to accepting the offer to expand Medicaid to everyone under 130 percent of the FPL, this strategy was costly to Wisconsin taxpayers. However, it allowed Governor Scott Walker to brag that he was the only governor to offer insurance to everyone while refusing the Obamacare subsidy to expand Medicaid. Unmentioned, of course, was that this strategy was available only because the Obamacare exchange made subsidized insurance available to those who were forced off Medicaid.

Eligibility of Uninsured in Wisconsin

What would be the effect on the people whose income is between 100 percent and 130 percent of the Federal Poverty Level—those who would have qualified for Medicaid under the Obamacare expansion but instead were encouraged to buy insurance on the exchange? First, it is worth noting that we do not know how many of those dropped from Medicaid actually gained coverage from other sources.

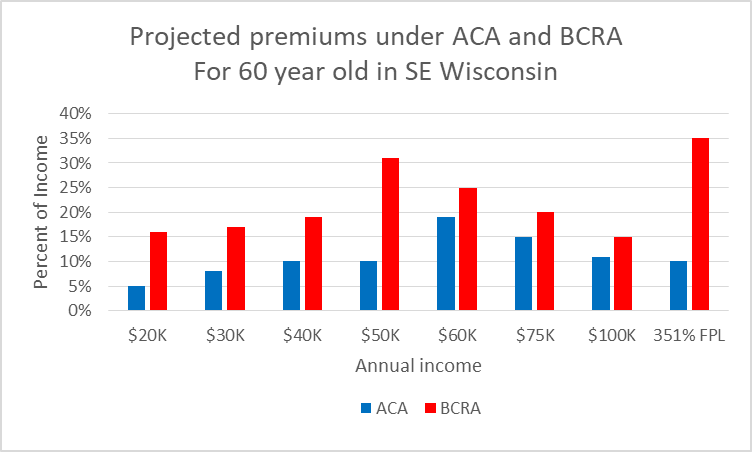

The Kaiser Family Foundation has published data on projected net premiums for each county in the U.S. broken down by income, age, and the type of plan chosen. The chart below shows the estimated premium after subsidies for a 60-year-old living in Southeastern Wisconsin and choosing the mid-level or “silver” plan. The blue columns are the net premium under the Affordable Care Act (Obamacare); the red show the net premium under the Senate bill. For someone making around $50,000 the premium would consume almost a third of that person’s income. It is likely that many people in their 50s and early 60s would find the premiums unaffordable under the Senate bill.

Projected premiums under ACA and BCRA for 60 year old in SE Wisconsin

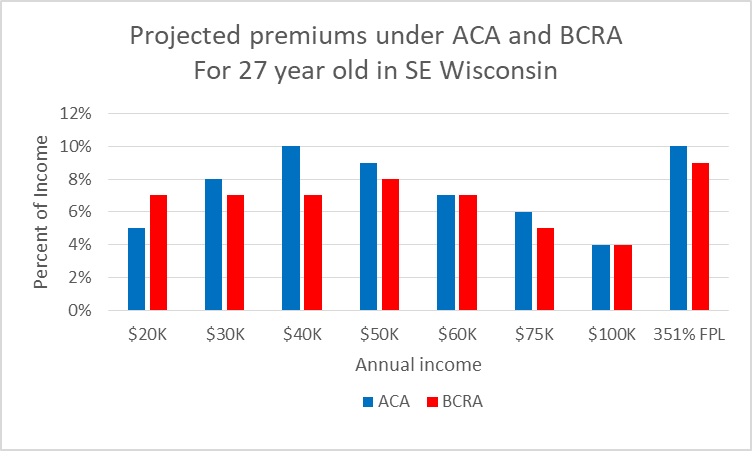

At first blush, the Senate bill favors young people. As shown below, for them the net premium would be lower sometimes and higher other times than today, depending on their income.

Projected premiums under ACA and BCRA for 27 year old in SE Wisconsin

But this comparison ignores the loss of “cost sharing subsidies” that help with deductibles. Under present law, the federal government requires insurance companies to reduce deductibles for low-income people. The government in turn subsidizes the insurance companies for their loss of income. Under the Senate bill, these subsidies would be eliminated starting in 2020.

The CBO concludes that few low-income young people would purchase insurance under the Senate plan:

Under this legislation, starting in 2020, the premium for a silver plan would typically be a relatively high percentage of income for low-income people. The deductible for a plan with an actuarial value of 58 percent would be a significantly higher percentage of income—also making such a plan unattractive, but for a different reason. As a result, despite being eligible for premium tax credits, few low-income people would purchase any plan, CBO and JCT estimate.

Thus the Wisconsin residents who lost Medicaid coverage because they were slightly above the FPL would likely end up without coverage.

The CBO report also concludes that neither the continuation of Obamacare nor its replacement by the Senate bill is likely to lead a “death spiral” in which only sick people buy insurance, leading to higher premiums and an ever-sicker insured population until the whole system collapses. It does warn, however, about insurers leaving the market under Obamacare:

Several factors may lead insurers to withdraw from the market—including lack of profitability and substantial uncertainty about enforcement of the individual mandate and about future payments of the cost-sharing subsidies to reduce out-of-pocket payments for people who enroll in nongroup coverage through the marketplaces established by the ACA.

The CBO does not mention that the Trump administration appears to be deliberately creating uncertainty about enforcement of the individual mandate and about future payment of the cost-sharing subsidies. Presumably this is so that the administration can claim that Obamacare is failing.

After listing uncertainties, the CBO concludes:

Despite the uncertainty, the direction of certain effects of this legislation is clear… the amount of federal revenues collected and the amount of spending on Medicaid would almost surely both be lower than under current law. And the number of uninsured people under this legislation would almost surely be greater than under current law.

From a conventional political viewpoint, the push by Donald Trump and the Republicans to repeal Obamacare or replace it with a plan that vastly increases the number of people without coverage is puzzling at best. The people most likely to lose affordable coverage skew heavily towards those who put Trump in office—middle aged and middle income.

A week before he took office, Trump gave an interview with the Washington Post, in which he promised, “We’re going to have insurance for everybody. There was a philosophy in some circles that if you can’t pay for it, you don’t get it. That’s not going to happen with us.” He promised to “not have people dying on the street.”

But dying is one of the risks of losing insurance coverage. A paper published this year estimated there would be one life saved for every 239 to 316 adults gaining coverage. Applying this range to estimates of the number of Wisconsinites losing coverage under the Senate or House version of Trumpcare results in an estimated additional 1,000 deaths per year in Wisconsin.

The effects of taking insurance away are not limited to mortality. As a recently published paper in the New England Journal of Medicine notes, having insurance affects financial stability, access to care, chronic disease care, and well-being and self-reported health. Whatever one thinks of the morality of the proposed plan, its negative outcomes cannot be good for Republicans’ political success.

Data Wonk

-

Will Wisconsin’s Gerrymandered Congressional Map Be Overturned?

Jul 1st, 2026 by Bruce Thompson

Jul 1st, 2026 by Bruce Thompson

-

How Partisan Are Wisconsin’s Members of Congress?

Jun 24th, 2026 by Bruce Thompson

Jun 24th, 2026 by Bruce Thompson

-

Why Are So Many Republican Legislators Quitting?

Jun 17th, 2026 by Bruce Thompson

Jun 17th, 2026 by Bruce Thompson

Bruce how about the status quo. If your on Medicare you actually pay about 10 percent of your costs. The other 90 percent is thrown on the working class. So right there about 10 percent of our citizens pay near nothing for their coverage. The largest generation the millennials, are mainly on mommy and daddy’s plan not til their 25 but Obama changed it to 27 years of age. So the largest generation is shielded from the real costs of health care. Then there are the “poor” which consists of working and not working. They to pay next to nothing for a Cadillac plan paid for by the working class.

Jason, Jason, Jason…

This article is about Medicaid and you posted about Medicare. Do you even understand the difference?

As to your claim that people on Medicare only pay 10% of its cost…

Medicare has 3 parts: A—Hospitalization; B—Doctors, tests, etc; and D—Prescription drugs. (There is also a Part C, but that’s just an all-in-one combination of the other 3 parts.)

People on Part A, pay 100% of the cost (80% through a lifetime of “Medicare tax” deductions), and the other 20% either out-of-pocket or via private-sector Medigap insurance (which is not subsidized whatsoever).

People on Part B pay 45% (25% deducted from their Social Security check, and the other 20% again either out-of-pocket or via unsubsidized, private-sector Medigap insurance.

People on Part D also have monthly premiums and co-pays, but I’m not sure how much of the total costs those people pay, but I’m sure it’s more than 10%.

Bruce where do you come up with these fairy tales. 1,000 deaths per year? Where did you pull that out of your butt? we have not had Medicaid money, extra thanks to scott not jamming us into that mess. Trump should have obamacare repealed and then send the money back to us to put into Badgercare and we would be far better off.

Feds, Bruce loves them, but they cannot run a whore house in the yukon at the height of a Gold Rush.

Wisconsin Conservative whoever you are If you do not have insurance you can go the emergency room but the last time I checked emergency rooms DO NOT treat cancer or diabetes or the host of other diseases that KILL people. Either we are a society that cares about our fellow citizen or we are a society where everyone is on there own.

I guess if we attempted to make it logical we would start with people and then those with insurance and those without insurance. Now the trick is to cover all those without insurance. I guess you would just say too bad or is it TS. Peace

Tom D is correct. Both Medicare and Medicaid are examples of single payer systems, but they target different audiences. Medicare pays medical bills for people over 65. Most recipients of Medicaid are under 65, but there are exceptions. For instance, people needing long term care are eligible for Medicaid once the exhaust their assets.

Obamacare has a number of provision, including the requirement stay on their parents’ plan until they pass age 25, the reforms to the nongroup market (including the exchanges), and the Medicaid expansion. All three contributed to the decline in the uninsured rate, but when people talk about Obamacare, they are often considering only the exchanges.

Republicans in both branches of congress need to fess up to the fact that repealing the ACA would be catastrophic to many millions of citizens in this country. Despite 7 years of trying to sabotage what they derisively called Obamacare, what they could not sabotage has resulted in health insurance for many millions who had not previously had health insurance. The ACA also reduced the rise of the cost of health insurance. Get real, reactionaries: own up to the fact that you have been wrong on the ACA for 7 years, and try to write legislation that results in more affordable health insurance for more citizens. Smart people acknowledge mistakes, and they make corrections.

Out right repeal would only affect 3 million. So dump the mess and give money to states. For reference on the 3 million see Dick Morris.

Too many think that ACA was the sum total of healthcare reform. It was not. It was the first step. It will take a great deal more to get the US Healthcare system working effectively and efficiently. That is not to say that undoing the ACA is the right move either. I believe both the House and Senate bills are pure economic folly.

The US spends nearly 17% of GDP on healthcare. Compare that to Canada, which spends 11%. However, the outcomes we get are significantly poorer than that of Canada, the UK, France, Germany and most other industrial nations. We spend more but we get less for the money spent. If we return healthcare to pre-ACA, which is what both House and Senate bills essentially do, healthcare inflation will run rampant. That will have an impact on our competitiveness globally, because our healthcare costs are added to the cost of doing business in this country.

How much harm–how many people have to lose coverage, lose their lives, jobs, homes, businesses–before we come to the realization that a market-based healthcare system is choking the economic life of this country?

Baloney. Health care outcomes are much better in USA. Canada does not have single payer but is a fourpart program with a;large numbers of private pays. When have you heard of anyone leaving USA to go to Canada, Germany, UK, France fro treatment?

Fact is the JCHAO did studies on these systems and none of them passed our standards for quality. Mary kay is silly.