ACA Premium Costs Rose 40% in Milwaukee

How and why ACA marketplace rates rose so high in Wisconsin and the nation.

Ascension Columbia St. Mary’s Hospital. Photo by Jeramey Jannene.

The issue of the day is affordability. Both parties seem to agree on that, while younger generations of Americans complain that things taken for granted by older generations are unaffordable to them. It is surprising, therefore, that Republican members of Congress seem intent on making health care unaffordable to more people.

Between 2020 and 2025, average premiums on the Affordable Care Act marketplace grew at the rate of 2% per year. This rate of growth was much lower than the 4.5% growth of employer premiums or 6.3% in national health expenditures. It was also much less than the rate of inflation. Why was the rate of growth so low?

Part of the explanation seems to be the structure of the marketplace. Government subsidies to plans on the marketplace are set to the second-lowest-cost plan. Plans costing significantly more than this amount are likely to get very low market share. Thus, there is a major incentive to drive down the price of each plan’s premium.

In addition, enrollment has grown in recent years, broadening the risk pool.

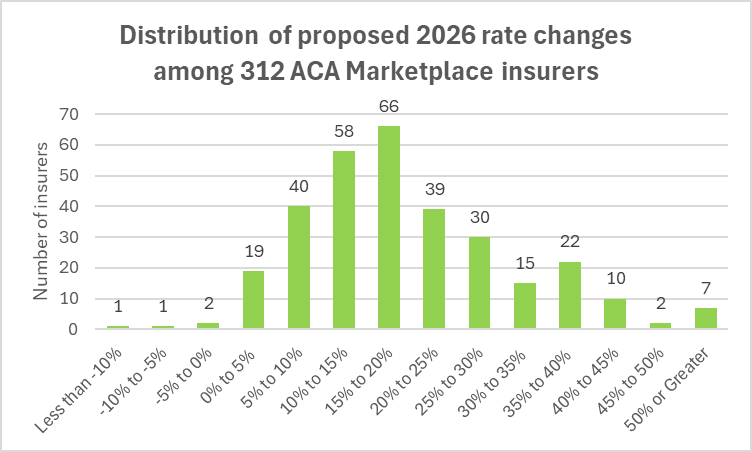

But in 2026, the story dramatically changed. Rather than an annual increase averaging 2%, the average premium price jumped to more than 20%. The next graph shows the distribution of proposed 2026 rate changes among 312 ACA marketplace insurers across the nation. This is based on analysis by KFF (formerly the Kaiser Family Foundation).

Distribution of proposed 2026 rate changes among 312 ACA Marketplace insurers

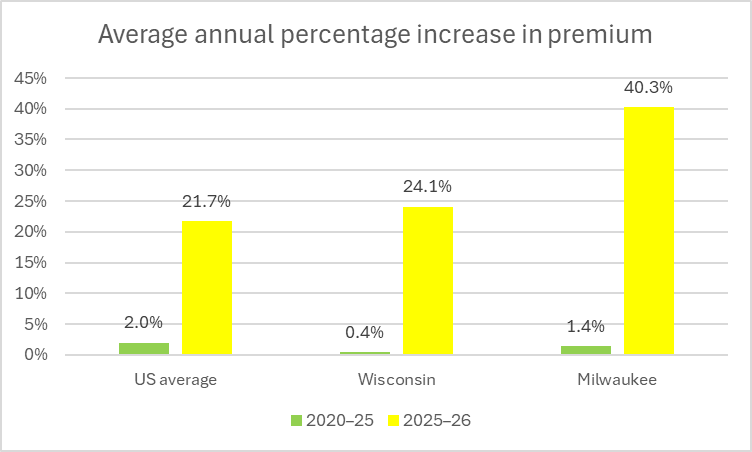

The next chart shows the magnitude of the jump in premium cost. Annual growth rates for 2020-25 are shown in green and those for 2025-26 are shown in yellow. Average U.S. cost increases grew from 2.0% to 21.7%; average Wisconsin cost increases grew from 0.4% to 24.1%, and for Milwaukee they jumped from 1.4% to a whopping 40.3%. (These numbers were calculated by the Urban Institute under a grant from the Commonwealth Fund.)

Average annual percentage increase in premium

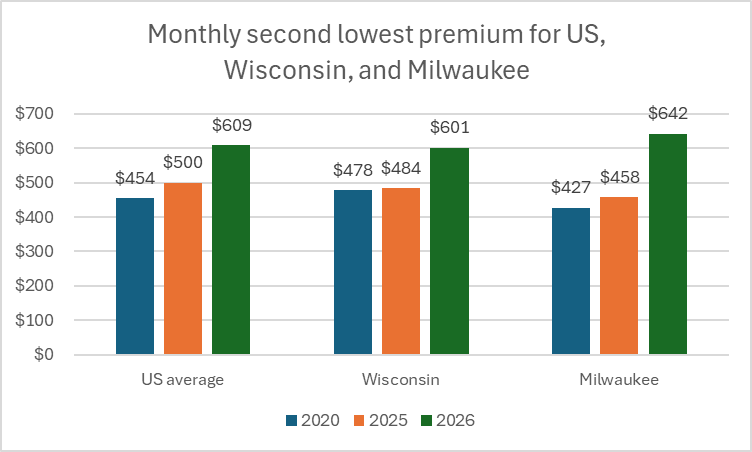

The next graph shows the monthly premium in 2020, 2025, and 2026 for the U.S., Wisconsin, and Milwaukee.

Monthly second lowest premium for US, Wisconsin, and Milwaukee

That’s an average annual increase of $1,308 nationally, $1,404 for Wisconsin and $2,208 for Milwaukee. What accounts for those extraordinary increases in premium growth between 2025 and 2026? The Republican Congress took two major actions affecting health care in 2025: the passage of H.R. 1, the so-called “One Big Beautiful Bill Act,” and the refusal to extend the enhanced tax credits.

Both actions (or nonactions in the case of enhanced tax credits) increased the uncertainty experienced by insurance companies in 2025 when they tried to price out their plans for 2026. Clearly there would be lower enrollment as more individuals would decide that health insurance had become unaffordable, resulting in an increase in the number of Americans without health insurance. But while the direction of the effect is clear, its magnitude is uncertain.

Another likely outcome was a worsening of the risk pool. Faced with increased prices, the healthiest individuals were the most likely to forgo insurance.

In addition, the One Big Beautiful Bill Act increased the paperwork faced by participants in these programs, resulting in some number of people being thrown off these programs for failure to submit the needed documentation.

What is the story that the data show? Over the 2020-25 period, premiums were actually declining in real terms. This was true for the nation, with a nominal growth rate of 2% per year, well less than the inflation rate. It was even more true of Wisconsin and Milwaukee, with growth rates of 0.4% and 1.4% respectively. To remain competitive, insurers had to reduce their premiums.

In 2025, when setting premiums for 2026, insurers faced an uncertain cost environment. Both the Big Beautiful Act and the end of the enhanced tax credits were certain to result in a loss of enrollees. This loss would be greatest among the healthiest people, worsening the risk pool.

Faced with this uncertainty, it is not surprising that the average premium jumped in 2026 or that four of the seven firms offering plans in Milwaukee decided to leave this market.

If you think stories like this are important, become a member of Urban Milwaukee and help support real, independent journalism. Plus you get some cool added benefits.

Data Wonk

-

The Irony of Trump’s SAVE Act

Apr 22nd, 2026 by Bruce Thompson

Apr 22nd, 2026 by Bruce Thompson

-

Who Do You Trust to Conduct Elections Fairly?

Apr 6th, 2026 by Bruce Thompson

-

Is Non-Citizen Voting a Real Threat to Elections in Wisconsin?

Mar 18th, 2026 by Bruce Thompson