Is Obamacare Failing?

Rhetoric aside, what does the data show?

Former Health and Human Services Secretary Kathleen Sebelius and President Barack Obama. Official White House. Photo by Pete Souza.

The Milwaukee Journal Sentinel’s Sunday Crossroads section had two articles with diametrically opposed takes on the Affordable Care Act, commonly called Obamacare. JS columnist Christian Schneider declared the ACA all but dead. A separate column from the Washington Post’s Catherine Rampell notes the act’s successes.

Recent decisions by United Healthcare and other insurers to leave the federal healthcare market have raised alarms, giving hope to opponents of the act like Schneider and Donald Trump. What can we predict about events in 2017 and beyond, as to whether the ACA is in trouble?

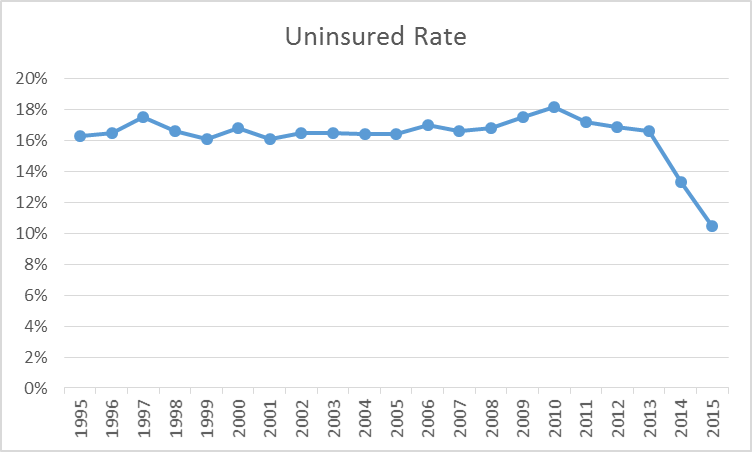

For decades the number of Americans without health insurance had been stuck between 16 and 18 percent. The ACA succeeded in its primary goal, of significantly reducing the number of Americans without health insurance. As of early 2016, an estimated 20 million additional individuals have gained health coverage as a result of the ACA. As the graph below shows, this translates into a substantial drop in the percentage of people under age 65 without insurance. (Other surveys have found similar results. Gallup estimates the uninsured rate fell from 18 percent in the first quarter of 2013 to 11 percent in the first quarter of 2016.)

Uninsured Rate

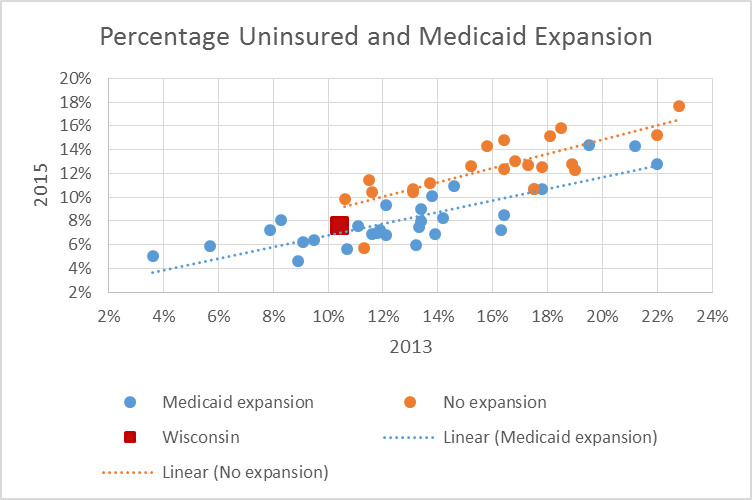

The drop in the rate of uninsured varied widely from one state to another. One important factor was whether the state expanded Medicaid to cover everyone making less than 138 percent of the poverty level. As the chart below shows, on average, states expanding Medicaid (shown in blue) had bigger reductions than those choosing not to expand.

Percentage Uninsured and Medicaid Expansion

Wisconsin (shown as a red square) is something of a special case, having rejected expansion money while opening Medicaid to anyone making less than 100 percent of the poverty level (mainly adults without children). To make room for them, parents making more than the poverty level were expected to buy subsidized insurance through the federal exchange. Based on its 2013 rate, Wisconsin’s 2015 rate of uninsured falls between states not expanding Medicaid and those expanding it.

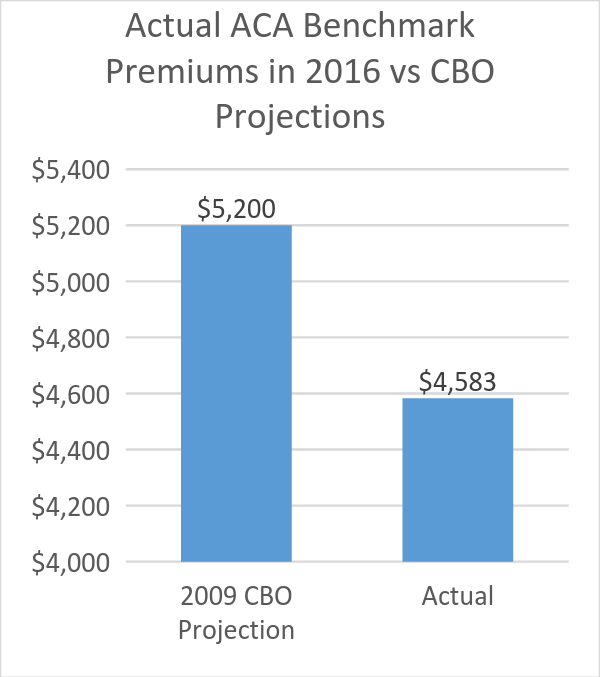

Did the ACA cause a rise in health costs, as Schneider seems to charge? For many years medical costs have been rising at a much greater rate than the general cost of living. Even the most enthusiastic advocates of the ACA did not expect it to cause a cost decline; rather, the hope was the growth would start to decline. Based on a number of different measures, that seems to have happened. For example, the Henry J. Kaiser Foundation found the average premium in 2016 was substantially less than the estimate for 2016 that the Congressional Budget Office used in 2009, before the law took effect. (Note that economists are uncertain as to how much of this decline is due to the ACA as opposed to other factors.)

Actual ACA Benchmark Premiums in 2016 vs CBO Projections

How much will average premiums of the exchanges rise in 2017 compared to 2016? Without disclosing his sources, Schneider claims Wisconsin’s average rates will rise anywhere from 16 percent to 30 percent.

The only systematic analysis that I have discovered comes from the Kaiser Foundation. It is based on proposed rates in the 17 largest cities in 16 states and the District of Columbia. None of those cities is in Wisconsin.

It appears that many insurance companies underestimated the cost of policies offered on the exchanges, accounting for both the withdrawal of several companies and higher price increases for next year. One of the causes of this under-estimate is that the companies misjudged how sick the population would be. At the extreme, this raises the specter of “adverse selection”: as prices rise only sick people buy insurance, causing further price rises, leading to a meltdown of the market.

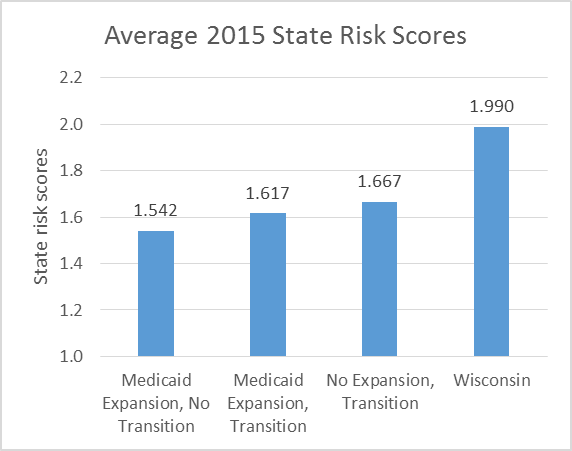

To assess this risk, the government has developed risk scores based on the age, sex, and diagnoses assigned to each enrollee in individual and small group market plans. These scores were developed to compensate insurers whose population was less healthy than average. In a recent report the Kaiser Foundation examined the effect of two state decisions on the average risk scores of the population in that state’s exchange.

The two state decisions were:

- Whether or not to expand Medicaid to cover everyone under 138 percent of poverty. Not expanding Medicaid allowed those making between 100 percent and 138 percent to go into exchange and get a subsidy.

- Whether to allow people to keep their previous insurance policies. Responding to political pressure, the Obama administration allowed states to seek a waiver to allow an extension of such policies to continue to the end of 2017.

Average 2015 State Risk Scores.

As the graph above shows, on average states which expanded Medicaid had lower risk scores than those which didn’t expand Medicaid. This result is not surprising, since poor people tend to be less healthy. Perhaps poor health interfered with holding a job. Conversely, a lack of resources meant that their health problems weren’t addressed.

Another study compared the cost of exchange plans in counties in states that expanded Medicaid with adjacent counties in states that did not. Included were Wisconsin counties bordering Michigan and Illinois. It found that “Marketplace premiums are about 7 percent lower in expansion states, controlling for differences across states in demographic characteristics, pre-ACA uninsured rates, health care costs, and state policy decisions other than Medicaid expansion…”

While Wisconsin’s abnormally high risk score can be attributed to its decisions to not expand Medicaid, this doesn’t fully explain the difference. Partly it may reflect our older population; older people have more health problems. Also, prior to the ACA Wisconsin had one of the lower rates of uninsured, possibly implying that those not covered had particularly challenging health issues.

Overall, the ACA has been a success in bringing down the number of people without health insurance. As with any new, complex program it has glitches. Looking to the future, one question is whether the political will exists to fix the glitches or the markets will be left to work around them.

Even if the political will doesn’t appear, it seems unlikely the ACA will suffer a meltdown. But plans on the exchanges may offer more limited provider networks as insurance companies compete on price. It also seems likely that those people willing to pay more for less restrictive networks tend to be less healthy. As a result, these plans are likely to evolve to look more like Medicaid and less like Medicare, with more limited coverage.

As companies such as United Healthcare leave the marketplace, other organizations with experience living with the much more austere payments offered by Medicaid may take their place. An example is the recent announcement by Children’s Community Health Plan that that it would be offering policies on the exchange. Children’s already offers Medicaid plans.

Extending the number of states that offer Medicaid to everyone making less than 138 percent of poverty is likely to be a longer slog. The potential beneficiaries are known for not being politically active, so they are easy for politicians to ignore.

To the extent that Republicans have been willing to suggest alternatives to the ACA, they have turned out to be non-solutions. An example is the proposal to allow people to buy health insurance across state lines. The result would lead to insurance companies establishing their base in the state with the weakest regulations and selling insurance nationwide, much as credit card companies are based in South Dakota or incorporations take place in Delaware. It is ironic that those claiming to support states’ rights would desire a solution that would gut state regulation, leaving only federal requirements on health insurance policies.

In a less polarized political environment, adjustments to major legislation like the ACA would be routine. The unwillingness of people like Schneider and Trump to offer either adjustment to the ACA or a viable alternative is both a symptom and a cause of the polarization that makes solving problems so hard.

Data Wonk

-

Scott Walker’s Misleading Use of Job Data

Apr 3rd, 2024 by Bruce Thompson

Apr 3rd, 2024 by Bruce Thompson

-

How Partisan Divide on Education Hurts State

Mar 27th, 2024 by Bruce Thompson

Mar 27th, 2024 by Bruce Thompson

-

Will Wisconsin Supreme Court Legalize Absentee Ballot Boxes?

Mar 20th, 2024 by Bruce Thompson

Mar 20th, 2024 by Bruce Thompson

Apparently Bruce Thompson dare not speak the word “deductible”. This significantly rising health insurance cost to persons/households using their health insurance is not mentioned once in this supposed analysis. I believe Thompson knows better but is purposely deceiving his readers by omission like all good propagandists (or does he not know what he is writing about- you choose).

Here are two primary measures by which Obama repeatedly lied about this fiasco- Each household will save $2,500 under Obamacare- FALSE! If you like your plan, you can keep your plan- FALSE!

Between the deceit by Obama and his co-conspirators that concocted this trainwreck (or “craziest thing in the world” per Bill Clinton), and the failed promises, I would say like most Americans, Obamacare is a failure.

PS- If Obama had sold Obamacare as a businessman in the private market, he would be prosecuted for fraud.

PPS- Obamacare is destined for financial failure unless it is bailed out by the taxpayers. The numbers don’t lie, more failure ahead. Obviously for the co-conspirators, that’s not failure, that’s an opportunity to sell more lies. Why would anyone cooperate with a group that crammed-down their throats a fraudulant and failed product. Who wants to cooperate with lying hucksters to bail the hucksters out of thier disaster? One good thing about this disaster is that you get on record all the supposed “journalists” that are in the tank for the Dems. It will be fun watching the Dems and their toadies slowly slink away from Obamacare.

When you put it in all caps people take you a lot more seriously. That’s just science. I love it when people who repeat partisan talking points verbatim claim others are propagandists. The irony is lost on them. Now that is fun.

Will voting patterns be affected by the the Affordable Care act. Minnesota, Pennsylvania, Florida, Colorado and Nevada are seeing HUGE premium increases.

All you Baggers who rip on the ACA seem to be complaining about the private insurance companies charging too much in premiums, or not competing at all and pulling out of the exchanges. OK, sounds like the obvious solutions are to

1. Have the stabilization of expanded Medicaid and stop allowing governors like Walker to hurt their own constituents to accomplish….what, exactly?

2. Require competition on the exchanges, even when private industry fails to do so. Sounds like a public option to me, like what should have been in the original bill. And it’ll lower costs for most people while keeping insurance companies in line. They had thei chance, and they screwed it up with their greed.

Those are your options. Going back to the “good old days” of dropping people for pre-existing conditions and having twice as many people be uninsured IS NOT A LEGITIMATE CHOICE. And neither is the FREEDUM to be uninsured and make society pay for your ER and hospital visits, jacking up the costs for the rest of us due to your freeloading.

May be we should put the V.A. in charge of all of us. Then the federal government can really squeeze the private sector out of heath and medicine.

I love it when the Dems and their poodles can’t refute the widely known lies and fraud committed by their beloved Dem hucksters who concocted the Obamacare trainwreck. Instead they try to distract from the topic by pointing out inane things like the use of a few capital letters. Is that what you mean by serious? Please refute what I stated about the lies and fraud. Please refute what I stated about the omission of any mention regarding deductibles in this dishonest supposed analysis by Bruce Thompson.

The Dems had complete control of federal government when they enacted Obamacare in cahoots with the insurance companies and hospital companies. They completely own the Obamacare trainwreck. But they can never accept responsibility for their mess. It is always someone else’s fault. And they always have another new government program to solve the last government problem they started. Who keeps buying junk from hucksters that have already sold them junk?

PS- I notice the Dem poodles here are even trying to slink away from their beloved Obamacare by blaming others. I bet I am having more fun than the poodles.

Train wreck? Many people are covered,and health costs rose by the slowest amount in years in the 5 years after Obamacare was passed. I see Billy Bagger ignores those FACTS and whines about the handful of people who are getting the short end of the stick vs the millions who are better off.

I’ll take that “train wreck” any day of the week, and if we didn’t have self-absorbed jags like Walker trying to sabotage it, we’d be even better off.

C;mon Billy Bags. Show us your plan for reducing the rate of uninsured, keeping insurance companies in line, and improving the stability and performance of the economy. BRING IT SON! Someone’s buying junk from hucksters, alright, but it’s economic illiterates like you that are the suckers in question.

PS_ Obamacare was a compromise to keep the private sector in the health care game. Single-payer is what’s coming if you decide to keep screwing with this. I’m good with that, but I bet you’re not.

Sorry Jason but the Donald will be lucky to get much higher than 40% of the popular vote and 200 electoral votes.

Poodles? You come up with that all by yourself? That’s a sick burn. Bill I don’t think Obamacare is perfect and there’s perfectly valid criticism of it, but you aren’t interested in a discussion. Your first post makes it clear that you are here to throw bombs. Bruce has studied it a lot more than you have, and your point about deductibles doesn’t change that or impress much. All you’ve really done is engage in ad hominem attacks against him.

If there’s one grace note in the whole foul train wreck, it’s that the POTUS himself loves to call it “Obamacare,” self-absorbed narcissist that he is. I hope that moniker can be coupled to him for the rest of his natural life.

It may not make me feel any better about my skyrocketing deductible and soaring premiums, but one takes small pleasures where one can.

WashCoRepub you must be feeling pretty depressed after that debate. The Donald will not be able to Make America Racist Again. He’ll be lucky if he gets 200 electoral votes. That would be 200 more than the self-absorbed narcissist deserves. I’ll be taking way more than small pleasure in his defeat.

Blue Cross Blue Shield in Minnesota is getting 49 percent increase in premiums and they have a 60 percent market share for the coming year. An upper middle class family that recieves no federal assistance will get a family plan that goes from $1300 a month to $1900 a month plus deductible of $7800

What about non-rich people Jason? Or is your only concern for the wealthy?

Vincent, please define wealthy. Do you mean anyone not getting an Obamacare subsidy? Like anyone with a private sector middle-class income and who actually has to pay for their health insurance?

PMD-Get real- deductibles are significant real costs for anyone in the private sector that uses their health insurance on a regular basis. You don’t need to be impressed, you need to do the math. Please try to think for yourself, just google “Obamacare deductibles” and read. As to Bruce Thompson- he needs to be called out for dishonest reporting. Just because Bruce Thompson writes for a web site doesn’t make him honest or an expert. But if he is an expert, he is dishonest. And if he thinks he is being honest in his analysis, he is not an expert.

Jake- How do you define a handful- 50 million people? 75 million people? You obviously must be an economic genius if you think the Obamacare trainwreck, the supposed “Affordable Care Act”, is a success (that would be sarcasm in case you don’t get it). Please tell us oh economic genius why insurance companies are causing Obamacare to fail because they don’t want to sell insurance at a loss. And while you are at it, tell us why the publicly-funded health insurance cooperatives are failing across the country. Also, please specifically tell us what I have said that is economically illiterate.

Let’s hear it genius. And then while you are at that, please refute the lies and fraud that the Obamacare trainwreck was sold on. Tell us Obama and his co-conspirators did not say every household would save $2,500 on their insurance. Tell us that Obama and his co-conspirators did not promise that “If you like your plan, you can keep your plan.” And if you can’t refute that, then tell us why should we trust your hucksters for anything else regarding our health insurance. And please tell us who the Dems were compromising with when they enacted the Obamacare trainwreck. They controlled everything then. They completely own it along with supporters like you. Please tell us.

PS- Here is a definition for those that are open to learning something. Propaganda-“information, especially of a biased or misleading nature, used to promote or publicize a particular political cause or point of view”.

PPS-So can others call Obama a supreme jag if Jake is allowed to call Walker a jag? Is that now fair game on this site? After all, Obama created the Obamacare trainwreck, Walker just reacted to it. And editors- If Jake is allowed to call people “baggers”, can others use derogatory names of a sexual nature about Jake? Please let us know what the rules are, because if Jake wants to go gutter, I’m sure words can be found that would be appropriate for him.

Billy Bags- You rant and rave, but give no real numbers and have ZERO solution to the real problem of covering the uninsured and in stabilizing costs so people aren’t thrown into bankruptcy once they face a helth problem that their insurance won’t cover. Me and Bruce have shown that Obamacare have made progress in solving these problems, but all you do is bitch and offer ZERO in response, Billy Bags.

The reason some of these insurance companies don’t want to be part of the Obamacare exchanges is because free-market capitalism relies on profit, and there’s no profit to be had from dealing with that portion of the citizenry. Sounds like a need for single-payer or public option to me, because I feel humans deserve that stability, but I suppose your arrogant self just shrugs and says “Sucks to be them.” Niiiice.

PS- I really don’t care about your pwe-cious fee-wings, Billy Bags. Stop whining and start bringing sone decency, intelligence and solutions to the conversation instead of talk-show idiocy.

Why so angry Bill? The reality that Donald is going to lose and lose big really starting to sink in?

Vince look at the labor participation rate. We are all losing.

You are a condescending, grumpy, know-it-all Bill, but a right-wing propagandist you are not (so you claim). Just a prophet of the truth. Just the facts for you. In that case, will you admit that Obamacare has not been a disaster? That there are some real successes because of it? For example, “On the plus side, Obamacare expanded coverage for the working poor. It knocked out exclusions for pre-existing conditions. It eliminated annual and lifetime benefit caps. It requires coverage for preventive care. It extended coverage to age 25 for children under family policies.” http://www.startribune.com/there-are-six-actions-the-state-can-take-now-to-combat-health-insurance-costs/397670581/

The rate of uninsured is at a record low, in the single digits. That is progress. That is a good thing. Yes you are right, it has problems, but if you are not a propagandist and only care about facts, you have to concede that it’s not all bad. If you won’t admit that, you are a liar.

What have you lost Jason? A job? A home? If everyone is losing, that includes you. So what exactly have you lost?

PMD- You sound like the perfect Dem poodle. I know its tough to follow the program, let me help you PMD- I provided the definition because of my use of the term propagandist early on in describing Bruce Thompson, which this article fits to a T. PMD I do admit there are some good things about Obamacare, but its costs way exceed its benefits- not only to the working middle class that is primarily paying for it, but in terms of skewing employment toward part-time, disincentives for people to work, and the wasteful government spending that will result from its failure. That is one of the reasons why I made my original comment about Bruce Thompson’s shabby analysis- he omits major costs associated with the Obamacare trainwreck. And on top of that, it was sold using lies and fraud. I understand lies and fraud are standard operating procedure for Dems, but some of us are not poodles. But call me a grumpy know-it-all because I don’t like your big Obamacare trainwreck. Boo hoo.

Jake- Grow up, you sound like a 12 year old, and I noticed you didn’t address of the substantive comments I made. And yeah Jake, I’m evil incarnate because I’m not a righteous Dem poodle like you. Some of you Dem poodles are so imbred that your brains are scrambled. Why is it that I think your supreme righteous love for humans is a bit flawed? But Jake, I’m going to say something nice to you- I hope your kids don’t grow up to be like you.

Vincent- I’m surprised but not surprised by your comments. What does Trump have to do with anything here? And by the way, how do you define wealthy?

But let me say, overall it is going to be fun watching the Dems and their mindless followers eat the Obamacare trainwreck. Enjoy the death spiral.

There are impartial sources of information to use as a resource when considering the healthcare issues in this country. One of the best is The Commonwealth Fund.Org. The Commonwealth Fund is respected universally for the quality, accuracy and impartiality of it research. In grading nations for the cost and the outcomes of their healthcare delivery systems, the U.S. comes in dead last in almost every measure. The ACA is a relatively modest reform proposal that has as its primary shortcoming its reliance on our wasteful greed driven private health care insurance delivery scheme. When someone like Dr. Bill McGuire can retire from United Healthcare with a 1.2 billion dollar kiss goodby, “something is rotten in Denmark” to quote Shakespeare. (That is right -billion with a “b”) The ACA limits administrative costs to 20% of the premium dollar. Single payer countries and Medicare do the same thing for around 4%. In a civilized society in the 21 century, healthcare should be a right not a privilege, and greed should be the first thing to be eliminated from its functioning.

I don’t care if you dislike Obamacare Bill. That hardly makes you unique. It’s your tone. You’re so aggressive and angry. That’s not good for your blood pressure. I don’t want to see you end up on an Obamacare Death Panel. You are worthy Bill. Angry old white dudes are important too.

Daniel Golden- Good point about how the ACA’s flaw is its continued reliance on the private insurance industry to act decently and competitively. They have not, which makes a public option and/or single payer an obvioys solution.

Billy Bags- You’re getting the level of respect you have EARNED, son. Keep waiting for that collapse, Bubble Boy. You’ll be waiting a LONNNNG time. You still can’t refute the facts me and Bruce have shown, proving Obamacare has left things in a better place than they were 6 years ago. And your whining, talking points and name-calling don’t change those FACTS.

Billy- you need to understand that outside of your Bubble World, you sound like a child that isn’t man enough to understand real issues. Outside the Bubble, you actually need to know that “I’ve heard stories” isnt good enough. Put down the red Pom-Poms, turn off the AM radio, and learn something.

The contrast between the Scneider and the the Rampell pieces in the Journal Sentinel on Sunday could be instructive to us on this site. The Scneider piece was based largely on spin; the Rampell piece was informed by factual information. Flaws in the ACA notwithstanding, it is evident that the act has decreased the arc of increase in health insurance costs, and that it has resulted in a greater percentage of citizens here with health insurance.

The Bill M rants on Murphy’s well researched and well written post strike me as paranoid. He sounds like he has heard scary things from scary people. Jake calling him Billy Bags reminded me of some lines from Melville’s BILLY BUDD:

“The sea is deceitful, Billy: calm above, but underneath a world of gliding monsters – preying on their fellows … ” Take it easy, Bill; nobody wants to eat you.

Keep sticking with facts, Bruce, and we may one day have more reasonable dialogue.

Here is the headline on the Commonwealth Fund’s July report on healthcare in local areas: “New Commonwealth Fund Scorecard Finds Health Care Improving in Many Communities as Affordable Care Act Expands Access and Promotes Quality.” The sub-head goes on: “Despite Progress, Analysis of 306 Local Areas Finds Health Challenges Still Exist; Obesity Rates Rose in More Than 100 Areas and Preventable Death Rates Stagnated Almost Everywhere.”

It is certainly fair to talk about the remaining problems. But I would not trust anyone who talks only of the problems and ignores the accomplishments. The column in this morning’s J-S by Nathan Nascimento of the Koch-funded “Freedom Partners Chamber of Commerce” is squarely in the latter category.

The reason that some are so critical and distrustful of the outcome is the process by which it was conceived and the transparency/honest communication (or lack thereof) leading up to it— AND the assumptions baked into it. Many of us with backgrounds in business, actuarial science, economics (and even psychology and human behavior) could tell these assumptions were obviously flawed, right from the very beginning. Leaving me to conclude: If the program was devised so as to self-destruct financially in a few years, so that single payer coverage would ultimately be substituted as a “last resort” alternative — well done!